Filing a claim after a motor vehicle accident is more than just paperwork, it’s a legal and financial process that can significantly impact your recovery and future. Unfortunately, many accident victims make simple but serious mistakes that jeopardize their chances of getting fair compensation. Whether it’s missing a deadline, saying too much to an insurance adjuster, or failing to understand what their policy actually covers, these errors often result in underpaid or denied claims. On this page, we’ll walk you through the most common mistakes people make during the MVA claim process, and how to avoid them. By staying informed and prepared, you can avoid setbacks and protect your rights from the very beginning.

Unfortunately, based on your response, you may not qualify to file a claim. Most personal injury cases must be filed within two years of the accident, in accordance with the statute of limitations. Please consult with a licensed attorney to explore any possible exceptions or additional options.

One of the most damaging mistakes an accident victim can make is simply waiting too long to take the necessary steps after the crash. Time is a critical factor when it comes to both your medical recovery and your legal rights. The longer you wait to act, the more likely evidence will go missing, memories will fade, and deadlines will be missed.

Every state has a statute of limitations that defines how long you have to file a claim after a motor vehicle accident. These laws are strictly enforced, and if you fail to act within the allowed timeframe, you could lose the right to seek compensation entirely. What makes this mistake even more dangerous is that the deadlines vary depending on the type of claim, personal injury, property damage, or wrongful death, and are influenced by who the claim is being filed against (e.g., a private driver vs. a government entity). That's why understanding the timeline specific to your state is essential. To avoid missing your window, we recommend reviewing this comprehensive breakdown of claim filing timeframes, which outlines deadlines, exceptions, and what happens if you file too late.

After an accident, it’s common to feel a surge of adrenaline that masks the pain of injuries. As a result, many victims choose not to see a doctor right away, believing their condition isn’t serious or hoping it will improve on its own. This can be a costly mistake. Insurance companies often interpret delays in medical care as a sign that your injuries weren’t caused by the accident or weren’t serious enough to justify compensation. Even worse, untreated injuries can worsen over time, making both your health and your claim harder to manage. Immediate medical evaluation creates an official record linking your injuries to the accident and protects your health from hidden or delayed conditions like whiplash, internal bleeding, or concussions.

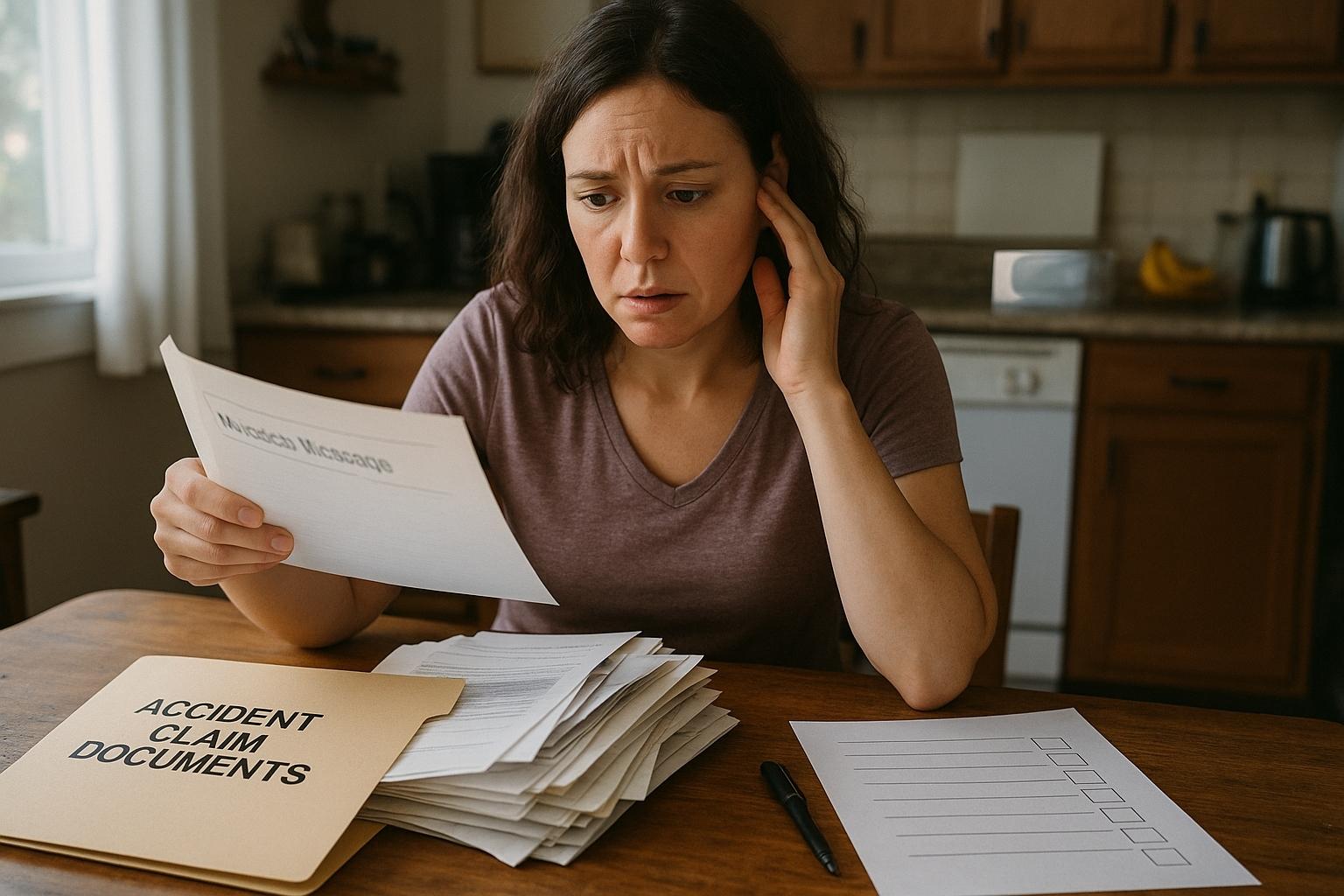

A successful claim isn’t based on your word alone, it’s built on documentation. Insurance companies need tangible proof of what happened, how you were affected, and what it will cost to make things right. Unfortunately, many claimants fail to collect or submit the right documents, which weakens their position and makes it easier for insurers to underpay or reject the claim.

Failing to gather critical documentation is one of the most common and preventable errors. Essential documents include the police accident report, photos of vehicle damage and injuries, repair invoices, hospital bills, diagnostic results, prescription receipts, and any written communication from your employer about missed work. Without these, the insurer may challenge the legitimacy of your claim or question the severity of your injuries. To help you get organized, we’ve created this practical guide to must-have claim documents that covers what to collect, when to collect it, and how to use it to support your case.

What you do at the accident scene can make or break your claim. It’s easy to feel overwhelmed, but forgetting to take photos, gather contact information from witnesses, or record road and weather conditions could seriously hurt your case later. These details provide visual evidence that can clarify how the accident occurred and establish fault, especially if the other driver disputes your version of events. If you’re physically able, take pictures from multiple angles, including damage to all vehicles, license plates, skid marks, and any relevant traffic signs. If you're unsure what should be documented, speak with a legal professional early in the process for guidance.

You pay for your insurance policy, but that doesn’t mean you know exactly what it covers. One of the most overlooked sources of compensation comes from your own auto insurance, especially if you’re dealing with an underinsured or uninsured driver.

Too often, drivers assume their coverage is limited to basic collision repairs, not realizing that add-ons like personal injury protection (PIP), medical payments (MedPay), or uninsured motorist coverage may also apply. These benefits can cover medical bills, lost wages, and even certain non-economic damages, depending on the state. If you’ve never reviewed your declarations page or spoken with your agent about these options, now is the time. Check out this deeper dive into overlooked insurance protections to discover coverage that could significantly strengthen your claim.

Although many claimants choose to handle their case independently, the truth is that MVA claims are filled with legal and procedural traps. What seems like a simple process can quickly become overwhelming, especially when insurers use technical language or stall tactics to avoid paying.

Unless you have experience negotiating with insurance companies or a deep understanding of personal injury law, you may not realize the full value of your claim, or how to get it. Without legal representation, it’s easy to overlook certain categories of compensation, like future medical care, diminished earning capacity, or non-economic damages like emotional distress. A qualified attorney can help you avoid these pitfalls, increase the size of your settlement, and ensure your rights are protected throughout the process. Learn more about why many people rely on legal support after serious accidents, especially in complex or disputed cases.

Even if you decide not to hire an attorney, you must follow the claim process carefully. Submitting an incomplete or incorrectly filled-out claim can lead to unnecessary delays or even denial. Common errors include missing supporting documents, using inconsistent language when describing the accident, or listing outdated contact information. To help you avoid these issues, we’ve prepared a detailed, step-by-step guide to filing your claim properly, including forms, timelines, and documentation requirements.

Receiving a denial letter can be frustrating and disheartening, but it’s important to remember that many claims are initially denied, only to be approved later through persistence and the right documentation.

In many cases, denials occur because of missing evidence, unclear accident details, or simple errors in the paperwork. If your claim has been rejected, don’t assume you’re out of options. Often, you can appeal the decision, submit additional medical records or accident reports, and even request a re-review with legal assistance. To get started, we encourage you to read this practical guide on overcoming a denied claim, which includes appeal steps and tips for strengthening your case the second time around.

The MVA claims process is full of potential pitfalls, but the good news is that most of them are avoidable with the right knowledge and preparation. By taking timely action, gathering the right documentation, managing conversations carefully, and seeking professional advice when needed, you can dramatically improve your chances of securing a full and fair settlement. MVAClaim.com was created to guide you through every step of this journey, providing resources, checklists, and expert insights to help you avoid mistakes and file with confidence. One mistake can be the difference between full compensation and a denied claim. Protect yourself by staying informed, organized, and cautious, and never hesitate to ask for help.

Unfortunately, based on your response, you may not qualify to file a claim. Most personal injury cases must be filed within two years of the accident, in accordance with the statute of limitations. Please consult with a licensed attorney to explore any possible exceptions or additional options.

© 2025 MVAClaim.com. All Rights Reserved.

**Disclaimer:** MVAClaim.com is a legal matching/referral service. We are not a law firm and do not provide legal advice. All legal services are provided by independent, licensed attorneys within our network. Your submission of information to MVAClaim.com does not create an attorney-client relationship. Results may vary depending on the facts and circumstances of each individual case. Past results do not guarantee future outcomes